- Preliminary

On 12 November 2018, the Telecom Regulatory Authority of India (“TRAI”)[1] published the Consultation Paper on Regulatory Framework for over-the-top (“OTT”) communication services (“Consultation Paper”).[2] This Consultation Paper was deemed necessary due to existing regulatory imbalances between telecom service providers (“TSP”) and OTT service providers, especially since the adoption and usage of OTT services have increased exponentially. The Consultation Paper aims to collate views of industry players, civil society, think tanks and other stakeholders to analyse the implications of the growth of OTT services, the relationship between TSP and OTT players, and any reforms that may be needed in the current regulatory framework.[3] The TRAI also held an open house discussion on the OTT regulation in May 2019[4]. While the TRAI had earlier announced that it would release its recommendations pursuant to the Consultation Paper by end of May 2019[5], they are yet to come out.

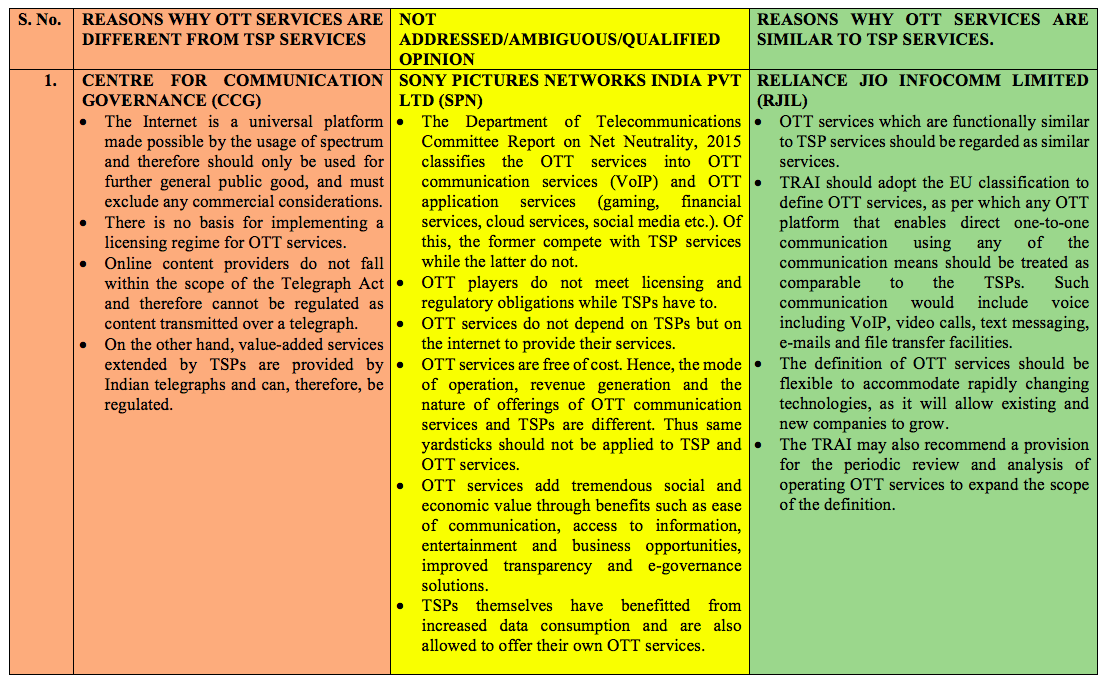

We have mapped the responses of the various stakeholders to the first question posed in the Consultation Paper, which is reproduced below:

“Which service(s) when provided by the OTT service provider(s) should be regarded as the same or similar to service(s) being provided by the TSPs? Please list all such OTT services with descriptions comparing it with services being provided by TSPs.”

We observe that stakeholder responses fall into three broad categories, namely stakeholders who believe that OTT services are similar to TSP services, stakeholders who have not addressed the question directly or have given vague or qualified responses and finally stakeholders who believe that OTT services are dissimilar to TSP services.

Our analysis is based solely on our understanding of stakeholders’ comments as submitted to TRAI and as published by the TRAI on its website. We have not reached out to any stakeholder for clarifications, nor has any stakeholder reached out to us. A total of 89 stakeholders submitted responses to the Consultation Paper. These 89 stakeholders comprise of 23 trade associations, 11 telecom service providers, 11 OTT service providers, 40 civil society members.

Per our analyses, 35 stakeholders (9 trade associations, 0 TSPs, 8 OTT service providers and 18 civil society contributors) believe that OTT service providers and TSP services are different and should be regulated differently; 27 stakeholders (9 trade associations, 1 TSP, 3 OTT service providers and 14 civil society contributors) have a qualified or ambiguous opinion or have not addressed the question directly; and 27 stakeholders (6 trade associations, 10 TSPs, 1 OTT service provider and 10 civil society contributors) believe that some OTT services may be similar to legacy TSP services or that they are essentially similar and therefore should be regulated similarly.

The tabulation of stakeholders’ positions is based on the responses of the respective stakeholders to the Consultation Paper. Given the breadth of this exercise, a few details may have been lost during the study of the responses. All suggestions and comments, to rectify any such omission(s) or error(s) are duly invited. Full submissions of all stakeholders are available here.

2. Stakeholders’ responses – an Overview

The analysis of the stakeholders’ comments finds that there are a few direct responses to the question of which OTT services should be considered similar to TSP services. Most stakeholders have given comments upon whether OTT services should be regulated, instead of which OTT service should be regulated. The mapping exercise has been done accordingly.

This exercise threw up some interesting trends. A majority of the stakeholders (35 stakeholders) are of the opinion that OTT services are not similar to TSP services, or have given qualified answers suggesting that while the two may be considered similar, regulatory parity between the two classes is not the way forward. A recurrent issue that came up in stakeholder responses is the lack of a clear definition of OTT services. Multiple stakeholders have sought to address this by referring to the European Union’s (“EU”) Electronic Communications Code (“ECC”) which distinguishes between Number-Based Interpersonal Communicational Services (“NB-ICS”) and Number-Independent Interpersonal Communicational Services (“NI-ICS”). OTT services in the EU fall under NI-ICS which are subject to light touch regulation. Other arguments for regulatory differentiation include different functional offerings; the fact that OTTs rely on TSPs to provide their services and so cannot be competitors; technical and infrastructural differences; ease of switching between different OTT services (as opposed to switching between TSPs, which is difficult); and the difference in business models. A majority of OTT service providers and civil society members have argued for a different regulatory environment for OTTs given that OTTs function as revenue generators for positive impact that OTTs have had on the revenue earned by TSPs through data consumption.

On the other hand, TSPs and cable/Direct to Home (“DTH”) companies (27 stakeholders) have vehemently argued for regulatory parity. The argument here is restricted to functional similarity and substitutability of services (i.e. if the services are functionally similar then they should be regulated similarly). Another proposal made by this camp is that all OTT service providers provide services which are similar to services provided under the unified licensing regime of the Telegraph Act, 1885 and hence should be regulated in a manner similar to that of TSP services.

There are a considerable number of responses (27 stakeholders) which give qualified answers such as which OTT services may be considered similar but why there is a strong argument for differentiation. Many stakeholders have simply stated similar and dissimilar services and have not given a reasoning. These have been categorised together with qualified responses since they do not contribute to explaining the overall trend.

We have documented the responses of all 89 stakeholders, with key takeaways from their submissions in a tabular format,

The full analysis can be accessed here.

This post is authored by Ratul Roshan, Associate, Ikigai Law with inputs from Tuhina Joshi, Associate. They were assisted by Srishti Sharma, Gayatri Gupta and Shretima Shrivastava, students at NALSAR, National University of Juridical Sciences and Rajiv Gandhi National University of Law, Patiala respectively.

[1] The TRAI was established in the year 1997 in pursuance of TRAI (Ordinance) 1997, which was later replaced by an Act of Parliament, named the Telecom Regulatory Authority of India Act, 1997, to regulate the telecommunication services. The website of the same is https://main.trai.gov.in/.

[2] The TRAI released the ‘Consultation Paper on Regulatory Framework for Over-The-Top (OTT) Communication Services’on 12 November 2018. The same is available at https://main.trai.gov.in/release-publication/consultation.

[3] TRAI, Consultation Paper on Regulatory Framework for Over-The-Top (OTT) communication Services, p. 3, 12 November, 2018. The same is available at https://main.trai.gov.in/sites/default/files/CPOTT12112018.pdf.

[4] TRAI, OHD on Consultation Paper on ‘Regulatory Framework for Over-The-Top (OTT) Communication Services, 20 May 2019, available at https://main.trai.gov.in/events/open-house-discussion/ohd-consultation-paper-regulatory-framework-over-top-ott-1.

[5] The Hindu Business Line, TRAI to finalise views on OTT services by May-end: RS Sharma, dated 23 April 2019, available at https://www.thehindubusinessline.com/info-tech/trai-to-finalise-views-on-ott-services-by-may-end-rs-sharma/article26921268.ece.